Contractor insurance built for Surrey trades. Not recycled from a national policy template.

Commercial General Liability (CGL), WorkSafeBC-aware advice, tools & equipment, and completed-operations coverage that responds when a job comes back years later. Family-owned brokerage since 1994. Same Fleetwood address. Same people answering the phone when a site emergency hits. Punjabi (ਪੰਜਾਬੀ) and Hindi (हिन्दी) spoken at the counter.

Tools stolen overnight? Texting is faster: 604-837-8710. Walk-ins at 150-8888 152A St, Surrey.

4,365 construction licences. Every one of them needs a broker who actually reads the contract.

Construction is 21% of all Surrey business licences. Your sub-contractor might need a $2M CGL, a Tools & Equipment floater, Builders Risk on an active job, and WorkSafeBC clearance before they walk on site. A generic commercial package doesn't assemble itself.

We've written contractor policies in Fleetwood since 1994. Electricians, plumbers, framers, roofers, HVAC, GCs, excavators, landscapers, concrete and masonry crews. We know what's in the coverage and, more importantly, what's not.

Who we insure

- Trades contractors Electrical, plumbing, HVAC, drywall, framing

- Roofers Residential & commercial, sloped & flat

- General contractors Renovation, custom build, commercial

- Excavation & earthworks Equipment-heavy operations

- Landscaping & concrete Seasonal & year-round crews

- Sub-trades & specialty Finishing, tile, flooring, painters

The roof was finished. The homeowners thanked him. A year later, the subrogation letter arrived.

A Surrey roofing contractor we'd insured for years replaced a roof on a single-storey home. Job completed. Homeowners paid. Handshake. Everyone moved on.

About a year later the roof started leaking. Water damage to the home's interior followed. The homeowners filed with their own insurer, who paid the repair costs — and then, as insurers do, subrogated against our client for what they'd paid out. A workmanship investigation deemed the installation faulty.

Here's where most contractors get caught: straight CGL covers ongoing operations. The part of a policy that responds to work you finished months or years ago is a different section entirely: Products & Completed Operations. If that section isn't scoped correctly at inception — with the right limits, the right retroactive date, and the right workmanship language — a subrogation letter like this one can become the contractor's personal problem.

Our claims team pulled the original inspection reports, the as-built documentation, and the specific work performed on that roof. We walked the adjuster through what was done, what the industry standard looked like, and where the policy applied. The Products & Completed Operations section responded.

What this story teaches

Most contractors buy a CGL policy and assume it covers everything. It doesn't. The section that covers work you've already finished — where the majority of contractor lawsuits actually come from — is Products & Completed Operations. If your broker hasn't specifically reviewed it with you, your policy may not respond the way you think it will. And once a claim lands, those limits are locked — there's nothing to fix after the fact.

Details anonymized to protect client privacy. Industry, claim pattern, and outcome are real. Every claim is different; past outcomes are not a guarantee of future results.

Your CGL aggregate and your Completed Operations sub-limit are not the same number.

A $2M CGL aggregate looks like plenty — until a workmanship claim lands a year after the job and only the Completed Operations sub-limit responds. That sub-limit is often a fraction of the headline number. Here's the difference.

CGL aggregate

The big number on the certificate.

- The total your policy can pay for covered claims in a policy year

- Commonly $2M, sometimes $5M for larger GCs or higher-risk trades

- The number a GC, lender, or municipal permit usually asks to see

- Covers ongoing operations while the work is in progress

Completed Operations sub-limit

The number that responds after the job ends.

- A sub-limit inside that aggregate — often a fraction of it

- Responds to workmanship claims that arrive months or years later

- Governed by the policy in force when the work was done, not the one in force when the claim arrives

- Where the majority of contractor lawsuits land — see the roofing story above

If your $2M aggregate carries only a $500K Completed Operations sub-limit, a workmanship subrogation can outrun your coverage long after you've been paid. We check the sub-limit, the retroactive date, and the workmanship language before you sign — not after the letter arrives.

The single most common contractor coverage gap

The single most common contractor coverage gap

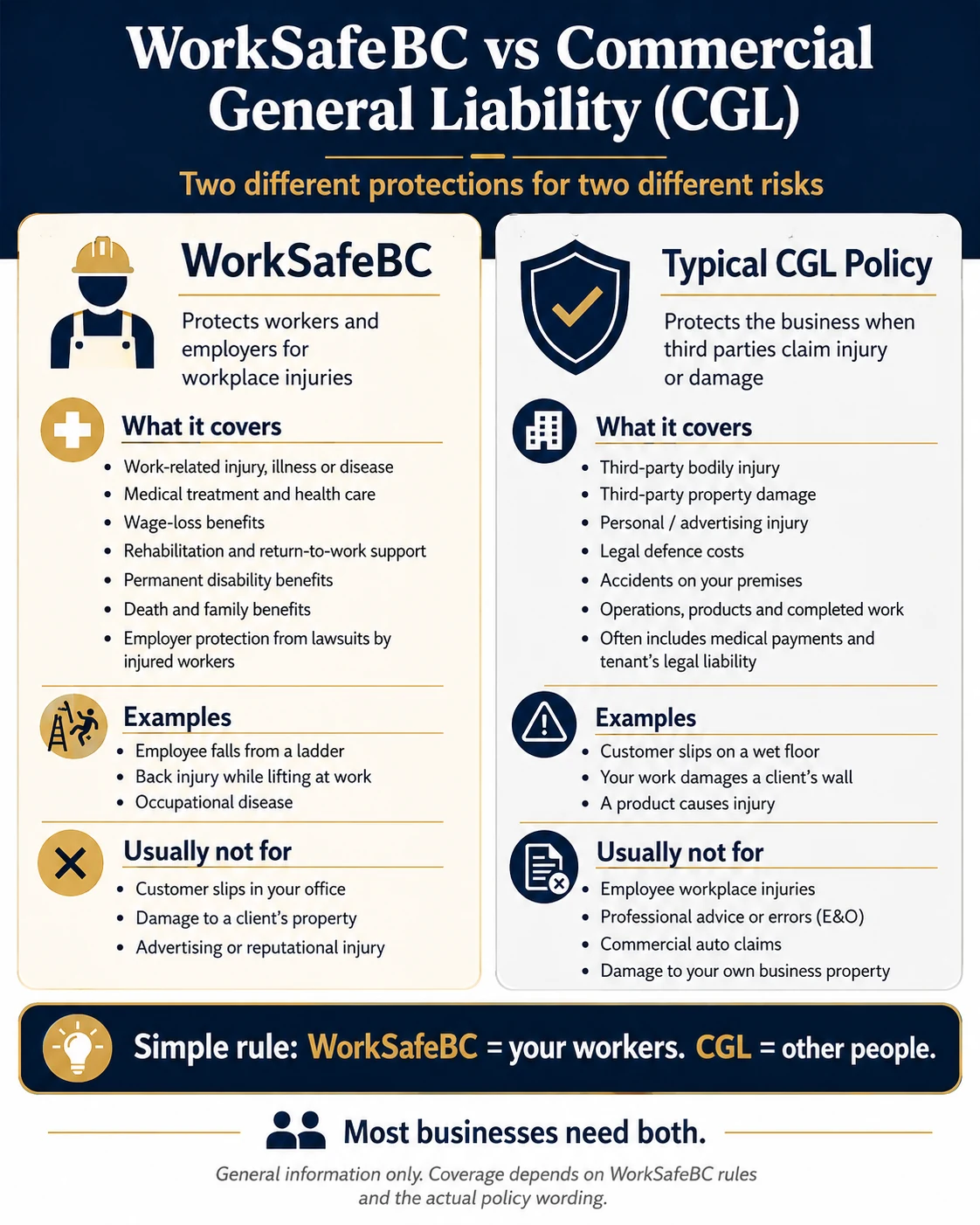

WorkSafeBC is not Commercial General Liability. You need both.

The most expensive assumption a Surrey contractor can make is that WorkSafeBC is "liability coverage." It isn't. Here's what each one actually does.

WorkSafeBC

Protects your workers.

- Mandatory for most BC employers and many sole operators

- Pays medical and wage-loss benefits when one of your workers is injured on the job

- No-fault — you don't have to prove the injury was someone's fault

- Does not cover third parties — customers, homeowners, the public

- Does not pay for property damage or legal defence

Commercial General Liability (CGL)

Protects everyone else.

- Covers third parties injured by your work or on your site

- Covers property damage you cause — homeowner's floor, neighbour's fence, hit water line

- Pays for your legal defence when you're sued

- Includes Products & Completed Operations for work you've finished

- Not mandatory by law — but required by most GCs, lenders, and municipal permits

If a roofer falls off your roof, WorkSafeBC pays. If a roof tile falls on your client's car, CGL pays. If your finished roof leaks a year later, Completed Operations under your CGL pays — if it's set up right.

Eight coverages we check before quoting any trade.

Not a shopping list. Every trade is different. But if your current policy doesn't specifically address these eight, ask why.

Commercial General Liability (CGL)

Third-party bodily injury and property damage. $2M limit is common, $5M for larger GCs or higher-risk trades. Includes legal defence costs, which can exceed the claim itself.

Products & Completed Operations

The section that responds to work you've already finished. The roofing story above happened here. Most contractor lawsuits arrive months or years after the job was done.

WorkSafeBC

Mandatory coverage for your employees' workplace injuries. Classification matters — a misclassified rate code can mean back-assessments after an audit.

Tools & Equipment Floater

Covers theft, damage, or loss of your tools and portable equipment on site, in the truck, or in the shop. Scheduled (listed) or blanket limits. Valuable for electrical, HVAC, landscape equipment.

Builders Risk / Course of Construction

Covers the structure being built during construction — fire, theft of materials, vandalism, water damage. Separate from the property owner's coverage. Required on many custom and multi-family projects. More on course of construction →

Commercial Auto & ICBC Fleet

Your trucks, vans, and trailers used for business. Correct ICBC rate class matters — Business-Terminal, Delivery, or Interstation affects what your claim looks like. We explain the differences.

Contractor's Pollution Liability

Standard CGL usually excludes pollution. For trades that disturb soil, handle fuels, or work around existing contaminants — excavation, demolition, certain HVAC and roofing work — a Contractor's Pollution Liability endorsement or standalone policy can respond to pollution incidents arising from your work. Whether you need it depends on your trade and your contracts. We flag it when your operation calls for it.

Subcontractor Liability & COI Verification

When you hire a sub, their CGL and WorkSafeBC clearance become part of your risk. If a sub is uninsured and something goes wrong, your policy may exclude work performed by uninsured subs. We help you verify subcontractor Certificates of Insurance, track WCB clearance, and structure OCIP / wrap-up arrangements on larger projects.

Depending on your trade and your contracts, we also scope:

- Builders Risk / Course of Construction for active projects

- Contractor's Pollution Liability for soil-disturbing and hot-work trades

- Owned / Hired / Non-Owned Auto for vehicles you use but don't own outright

- Inland Marine for materials and equipment in transit

- Equipment Breakdown for owned machinery

- Subcontractor OCIP / wrap-up on larger projects

- WorkSafeBC (WCB) clearance verification

Five ways a contractor policy collapses at claim time.

The problem is rarely having no insurance. The problem is having coverage that isn't set up properly. Every one of these is a failure pattern we've seen in Surrey. Every one is preventable with a 15-minute review.

-

Products & Completed Operations was never properly scoped

Your CGL might have a $2M limit — but only $500K of it attaches to Completed Operations. A workmanship subrogation lands 18 months after the job, and the number on the page doesn't cover the loss. We've seen this more than once — the roofing story above happened in exactly this section of the policy.

-

Sub-contractor exclusion was never flagged

A GC hires a sub who doesn't carry their own CGL. Something goes wrong. The GC's policy has an exclusion for work performed by uninsured subs — and the claim can be denied. Your hold-harmless agreement didn't help. Insurance responds to what's written in the policy, not what you meant the agreement to do.

-

Tools and equipment were under-scheduled or blanket-limited too low

Your truck gets broken into. $18,000 worth of tools gone. Your floater has a $5,000 blanket limit. The other $13,000 comes out of your pocket. We schedule expensive items properly so the policy matches what you actually own.

-

ICBC commercial rate class was wrong from day one

You're on "Business" rate class but actually running deliveries. An accident happens. ICBC can deny or reclassify the claim because the use doesn't match the class. No one explained the difference between Business-Terminal, Delivery, and Interstation when you bought the policy. We explain it on day one.

-

WorkSafeBC classification unit didn't match what you actually do

A post-incident audit reclassifies your operation into a higher-risk unit. Retroactive premiums are assessed. Your coverage was in place but the back-assessment becomes your bill. We audit classification against actual operations before it becomes an invoice.

Five failure modes, each catchable in a 15-minute review before a job starts or before renewal. Book the review →

What a contractor policy actually costs in Surrey.

No broker can quote you from a webpage. But here's the range most Surrey contractors land in, so you can see whether your current premium is reasonable.

Ranges are illustrative placeholders for planning purposes. Your actual premium depends on trade, revenue, payroll, claims history, coverage selected, and current market conditions. We'll give you a firm number, in writing, after a 15-minute review.

Some contractor risks need a market check before we can quote properly.

We can review most Surrey contractor policies within a 15-minute call. Some risks need an underwriter conversation first — recent significant claims, certain trade-and-height combinations, operations that span provinces, and risk profiles where the carrier appetite has shifted recently. We don't know the answer for those until we ask the market.

Here's what that means for you: call us anyway. If the risk needs a market check, we'll tell you in five minutes what we need to do, how long it takes, and whether it's worth the effort. If we can't place it at terms that work for your operation, we'll say so directly and point you to a specialty broker who can.

We'd rather spend five minutes telling you honestly than ninety minutes in a quote process that ends in disappointment. Your time on a job site is the most expensive thing you own.

Book a 15-Minute Contractor Coverage Review.

At the end of 15 minutes, you'll know exactly where your policy holds — and where it breaks. We take your current policy apart: Products & Completed Operations, Tools & Equipment, sub-contractor exclusions, ICBC rate class, and WorkSafeBC classification. We compare it against quotes from the markets that will entertain your risk.

- You call or text. We book a 15-minute slot — phone, video, or walk-in at Fleetwood.

- You bring your current policy. Email it, walk it in, or read it over the phone — and tell us about any GC contract or COI you're up against.

- We go through it line by line. Products & Completed Operations sub-limit, Tools & Equipment scheduling, sub-contractor exclusions, ICBC rate class, and WorkSafeBC classification.

- You get the written gap summary plus three competing quotes within two business days. Yours to keep.

Many reviews uncover at least one coverage gap the contractor didn't know existed.

Best time to do this: 30–90 days before renewal — ideally ahead of the spring municipal-permit rush or the year-end push, before the current policy is already being rewritten.

If you skip this, the next time you read your policy carefully may be after a claim — when it's too late to change anything.

No obligation. No sales pressure. No commitment to switch. If your current policy is strong, we'll say so — and you keep the written gap summary either way.

What we put in writing for contractors.

A missed COI breaks a job. A renewal shock breaks a quarter. Here's what we commit to in writing.

2-Hour COI Guarantee

Existing commercial clients with active policies: your Certificate of Insurance is delivered within 2 business hours during commercial desk hours (Mon–Fri, 8:30am–6:00pm). Complex COIs with multiple sections and policy numbers need accuracy — 2 hours lets us build it right the first time.

15-Minute Coverage Review

A side-by-side comparison of your current policy against quotes from the markets that will entertain your risk, plus a plain-English gap summary. You keep the written recommendation even if you don't switch. No obligation.

Answers in plain English.

Do I need WorkSafeBC and CGL before my next job starts?

Most GCs and most municipal permits require proof of both before you set foot on site. WorkSafeBC clearance shows your workers are covered; a Commercial General Liability (CGL) Certificate of Insurance — often naming the GC as additional insured — shows third parties are covered. For existing clients we can usually issue both quickly. Bring us the job details and any contract requirements and we'll tell you exactly what the GC or municipality is asking for.

Do I need WorkSafeBC if I'm a sole proprietor with no employees?

WorkSafeBC requirements depend on operation type. Self-employed proprietors with no workers may not be required to register, but most employers must. Even when WorkSafeBC itself doesn't require it, many GCs will require proof of registration before letting you on site. Personal optional protection under WorkSafeBC can also be worth the cost compared to private disability for trade-specific injury risk. We walk you through when you need it, when you don't, and what the cost looks like.

What's the difference between $2M and $5M CGL — and which do I need?

A $2M CGL limit is the industry baseline for most trades. A $5M limit is common for GCs, higher-risk trades, larger contracts, and work involving public buildings or multi-family construction. The cost difference between $2M and $5M is usually smaller than contractors expect. Your decision comes down to contract requirements, the scale of what you're working on, and your exposure to catastrophic loss. We explain the practical difference on a 15-minute review.

My GC's contract says "$5M CGL and the GC must be added as additional insured." What does that mean?

The GC is requiring that their company be named on your CGL policy as an additional insured for that project. It extends some of your policy's coverage to protect them against claims that arise from your work. It's a standard construction industry requirement. We issue the endorsement on your policy, produce the Certificate of Insurance showing it, and deliver it within 2 business hours for existing clients.

I had a claim last year. Will that mean I can't get insurance?

Having a claim doesn't automatically make you uninsurable. It affects what insurers will offer and at what premium. We have access to markets that specialize in contractors with claims history. The answer depends on what happened, how it was resolved, and your industry. Call us with the details — we'll tell you honestly what the market looks like for your profile.

My truck was broken into overnight and $14,000 of tools were stolen. What happens now?

File a police report immediately — insurers require it. Call us the same day. If you have a Tools & Equipment floater (blanket or scheduled), we start the claim process. One of our advisors — preferably the advisor who placed your coverage, or a senior advisor — stays on the line with the adjuster from first report to final cheque. If your limits are too low to cover the loss, that's a conversation we should have had before the break-in — and the reason we emphasize scheduling expensive items properly.

How fast can I get a Certificate of Insurance for a job site meeting tomorrow?

Existing Prime commercial clients with active policies: within 2 business hours, during commercial desk hours (Mon–Fri, 8:30am–6:00pm). New clients: same business day with complete information. Complex COIs with multiple additional insureds and specific coverage requirements take a little longer to build accurately — 2 hours is our commitment. If we miss the window for an existing client, we send you a $50 gift card.

My ICBC rate class changed after an accident. Is that normal?

Rate class can be reviewed after a claim if your actual use doesn't match what's on the policy. Commercial auto has several rate classes — Business-Terminal, Delivery, Interstation — and they aren't interchangeable. If you were on Business rate class but actually doing deliveries, ICBC can reclassify and reassess. We check rate class at placement and at every renewal to make sure the paper matches what you actually do.

Do you work with contractors who speak Punjabi or Hindi?

Yes. Members of our Fleetwood team speak English, Punjabi, and Hindi. Coverage reviews, claims advocacy, and Certificate of Insurance requests can all be handled in your preferred language. Ask for Kul, Kuljeet, or Seema by name.

What if my work is already covered by my GC's insurance?

The GC's policy protects the GC — not you. If something goes wrong with your work, the GC's insurer will often subrogate against you (come after you for the payout) just like the homeowner's insurer did in our roofing story. You need your own CGL and Completed Operations even when working under a GC. Treat the GC's coverage as protection for their business, not yours.

How do I switch to Prime if I'm mid-policy with another broker?

We usually wait for your current renewal to avoid mid-term cancellation penalties, but we start the review and quote process now. You bring us your current policy declarations page and a few details about your operation. Within 2 business days we produce a written comparison against the markets that will entertain your risk. You decide. If we're a fit, we handle the handover end-to-end — no day of missed coverage.

I work out of Cloverdale / Newton / South Surrey / Whalley — do you only serve Fleetwood contractors?

Our office is in Fleetwood but our contractor clients work across Surrey, Delta, Langley, White Rock, Coquitlam, Burnaby, and the Fraser Valley. The office address is where we are. The service follows wherever your projects run.

Why family-owned since 1994 matters for my business.

Over the past decade, many BC family brokers have been acquired by national consolidators and insurance-company-owned networks. Prime hasn't. Same Shergill family. Same Fleetwood address. Same names answering the phone. When your subrogation letter arrives, you call the same person who wrote the policy — not a national queue.

What's the difference between blanket and scheduled tools coverage?

A blanket limit covers your tools up to one shared amount, usually with a per-item cap. Scheduled coverage lists high-value items individually at their full value. If you carry one or two expensive items above the blanket per-item cap, scheduling them is often the difference between a covered loss and an out-of-pocket one. We review your tool list against your limits.

My certificate says $2M CGL — why might my Completed Operations limit be lower?

Your $2M is the CGL aggregate — the headline limit on the certificate a GC or municipality asks to see. Inside that aggregate sits a separate Completed Operations sub-limit, and it's often a fraction of the headline number — say $500K of the $2M. Completed Operations is the section that responds to a workmanship claim that lands months or years after the job ends. So a certificate can read $2M while the part that actually answers a post-job subrogation is much smaller. We check the sub-limit, the retroactive date, and the workmanship language before you sign — the two-number breakdown above walks through both numbers side by side.

What's a retroactive date on Completed Operations, and why does it matter?

Completed Operations responds to work you've already finished. A retroactive date sets how far back that coverage reaches. If you switch insurers and the new policy's retroactive date is set to the switch date, claims from older jobs may not respond. We check the retroactive date every time a contractor moves to a new market.

Does my GC's wrap-up (OCIP) policy mean I don't need my own coverage?

Usually not. A wrap-up or OCIP covers specific operations on a specific project, often only while you're on that site. It rarely covers your tools, your vehicles, your off-site work, or your Completed Operations after the project ends. Treat a wrap-up as project-specific protection layered on top of — not instead of — your own program.

A municipal permit needs proof of insurance by a deadline — how fast can you turn it around?

For existing Prime commercial clients with active policies: within 2 business hours during commercial desk hours (Mon–Fri, 8:30am–6:00pm). New clients: same business day with complete information. Send us the permit's exact insurance wording — limits, additional insured, any endorsements — and we build the Certificate of Insurance to match.

What our clients say about working with Prime.

Not every review below is from a contractor — but they show the service pattern trades clients care about: named advisors, fast answers, and long-term local relationships.

Service is excellent. I have been using Prime Insurance for ALL our insurance needs, from quads and trailers, through auto, home, and commercial liability. Kul Jr. knows me by name from the sound of my voice (or call display 🤣) and that makes me feel like a valued customer!

If you need auto, home or business insurance go see Kul at Prime Insurance. They have a professional team of agents that can take care of all your insurance needs. Been using them for almost 10 years.

Kul is the best at Prime Insurance! He has helped me with my personal vehicle insurance and insurance for my many vehicles for my businesses. Kul is always available to answer my questions and is quick to help. I highly recommend them!

Book the 15-minute Contractor Coverage Review.

We'll check Products & Completed Operations, Tools & Equipment limits, sub-contractor exclusions, ICBC rate class, and WorkSafeBC classification. Three competing quotes. Written in plain English. You keep it.

Prime Insurance

150-8888 152A St, Surrey, BC V3R 0V7

Retail counter: Mon–Fri 8:30am–9:00pm · Sat 8:30am–6:30pm · Sun & Stat Holidays 10:00am–5:30pm

Commercial desk: Mon–Fri, 8:30am–6:00pm

Get directions →