A second opinion for BC homeowners

Home Insurance in BC — Is Your Policy Any Good?

4.8★ · 600+ Google Reviews · Read them on Google

You’re probably not shopping for new home insurance. You already have a policy. What you actually want to know is whether it’s any good.

Whether the renewal that came in 18% higher is fair. Whether the gaps you’ve heard about — earthquake, overland water, the strata deductible thing — apply to your home. Whether you’re getting the discounts you should. Whether your policy would actually pay out the way you assume if something went wrong.

We can tell you. Bring us your declarations page. We’ll read it line by line, in 30 minutes, and tell you what’s covered, where the gaps are, and whether the BC market has a better fit for your home. No obligation. Honest answer either way.

Get a Second Opinion on Your Current Policy →

The trap most BC homeowners don’t know they’re in

BC home insurance changed in the last five years. Most homeowners haven’t caught up.

The numbers tell the story. Canadian severe-weather losses hit $8.55 billion in 2024 — the costliest year in Canadian history (Insurance Bureau of Canada). BC premiums rose 5.89% on average in 2025. Construction costs are up. And per industry research, nearly 80% of Canadian homes are underinsured — by an average of 27%.

Sources: Insurance Bureau of Canada / CatIQ (2024 catastrophe losses); MyChoice Financial (2025 BC rate analysis); Marshall & Swift/Boeck insurance-to-value research.

Here’s why that matters to you.

Your policy promises to rebuild your home. But if the dwelling limit on your declarations page is below about 80% of what a rebuild actually costs today, your Guaranteed Replacement Cost protection falls away. Even a partial loss — a kitchen fire, a bathroom flood, a burst pipe in the wall — gets paid proportionally, not in full. The rest comes out of your pocket.

We call this the BC Assessment Trap. Most BC homeowners anchor their dwelling limit to their BC Assessment value, because that’s the number they see every year. But BC Assessment is a property-tax calculation, weighted toward land value. It’s not what your home costs to rebuild. The two numbers can be hundreds of thousands of dollars apart.

What home insurance covers in BC. And what it doesn’t.

Your standard BC home policy covers four things.

- Building. Repairs or rebuilds your house — walls, roof, attached garage, built-ins — after a covered loss like fire, windstorm, or a burst pipe.

- Personal property. Replaces what’s inside — furniture, electronics, clothing, appliances. Watch the sublimits: jewellery, art, and bicycles usually have their own caps.

- Personal liability. Pays legal costs and settlements if a guest is injured at your home, or you accidentally damage someone else’s property. Most BC policies start at $1 million. $2 million is becoming the standard — court awards have moved.

- Additional living expenses. Pays for hotels, meals, and storage while your home is being repaired. On a major loss, 18 to 24 months of temporary housing isn’t unusual in BC’s rental market.

That’s the package. Broader than most people realize.

Now here’s what it doesn’t cover. Four big BC risks that aren’t in the standard policy. Each is a separate decision you make.

- Earthquake. BC sits on the Cascadia Subduction Zone. Optional coverage — usually as an endorsement. Deductible runs 10% to 20% of your dwelling limit — see the math below.

- Overland water. Heavy rain, river overflow, snowmelt entering from outside. Optional coverage — usually as an endorsement. (A burst pipe inside the wall is covered by the standard policy. Different category.)

- Sewer backup. Water or sewage coming up through your drains. Optional coverage — usually as an endorsement.

- Service line. The underground water, sewer, gas, and electrical lines from your house to the street. Your responsibility to maintain. Your repair bill if they break — unless you add the endorsement.

Four standard coverages. Four optional ones. That’s BC home insurance, end to end.

The four coverage tiers — and why the cheapest one usually isn’t the bargain it looks like.

The Insurance Bureau of Canada sorts BC home policies into four tiers. The tier sets what’s covered by default, before you add or remove a thing.

- Comprehensive. Building and contents covered for all risks except what’s specifically excluded. The strongest standard tier, and what most BC homeowners should carry.

- Broad. Comprehensive coverage on the building, narrower named-perils coverage on contents. A step down.

- Basic / named perils. Only the risks specifically listed are covered. Cheaper, narrower — sometimes suits seasonal or rental situations.

- No-frills. Offered by a few insurers for properties that don’t meet standard underwriting — older homes, past claims, vacancy. A way to get some coverage where the standard market says no.

We tell you which tier your home actually needs. Not which tier is cheapest.

Beyond the big four — the add-ons worth asking about.

The four optional coverages above are the ones that catch most BC homeowners out. A handful more are worth a question at review time: bylaw / code-upgrade coverage (rebuilding an older home to today’s code costs 10–25% more), scheduled personal property for jewellery, art, and bikes above the standard caps, equipment breakdown for sudden furnace or heat-pump failure, glass and identity-theft add-ons, a home-business extension, and umbrella / excess liability stacking $1M–$10M across home, auto, and rental. Which ones fit depends on your home — see the glossary below for the plain-English version of each. Not every home needs every one — that’s exactly what the second-opinion review sorts out.

Pick your product.

Home insurance in BC isn’t one product. It’s five — each with different coverage logic. Find yours below.

Or skip the sorting — get a second opinion first →

Not sure which one fits? Call us. Live in a duplex you own and rent out the other half? Have a basement suite plus a separate cabin on the Sunshine Coast? The 30-second answer is usually clear once we know how the property is structured.

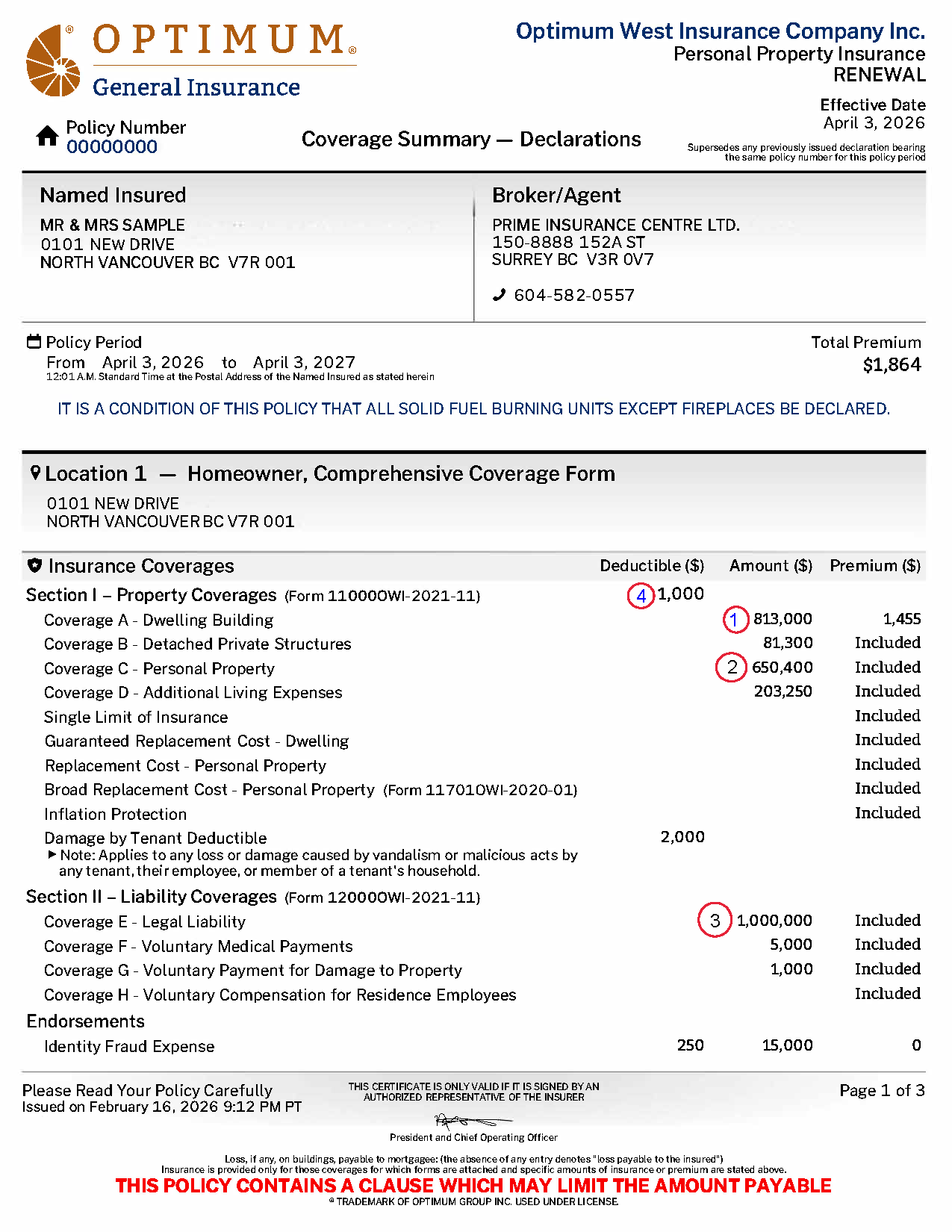

The four numbers on your declarations page.

Pull out your declarations page. It’s the one-page summary your insurer sends with every policy. Four numbers on it decide what you’re actually covered for. Most BC homeowners can’t tell you what any of them mean.

Here’s the four. The diagram above shows them on a real (anonymized) BC declarations page. The amounts shown next to each label below are from that sample.

Dwelling limit $813,000 — What the policy pays to rebuild your house. Has to match what a rebuild actually costs today. Recalculate every three years, and again after any renovation over $25,000. This is where the BC Assessment Trap lives — the single most common error on a BC home policy.

Personal property limit $650,400 — What the policy pays for what’s inside. Most carriers default to 70 to 80 percent of the dwelling limit. Sense-check this if you have meaningful contents. Most BC homes are under-counted.

Liability limit $1,000,000 — What the policy pays if someone sues you. $1 million was the standard for years. $2 million is becoming the standard — and the premium difference is usually small. Worth asking about.

Deductible $1,000 — What you pay yourself before the policy pays anything. Standard deductibles run $1,000 to $2,500. Earthquake deductibles are a different animal — 10 to 20 percent of your dwelling limit, which on a $1.5 million home is $150,000 to $300,000. Plan for it separately.

Now find your own declarations page and check yours against these four. If any number looks wrong, that’s the conversation we should have.

The BC traps that can restrict coverage at claim time.

These are the things other brokerages quietly leave out of their explanations. Each one of them has cost real BC homeowners real money.

The four-day winter rule. Most BC home policies say this: in heating season, if you’re going to be away from home for more than four days, you have to shut off the water at the main valve OR have a competent person check the home daily. If you don’t, and a pipe bursts while you’re away, the claim can be denied. CBC News has covered the BC denials, including cases of cancer patients away for extended treatment. The fix takes 30 seconds — call us before you go.

The 30-day vacancy rule. A different rule, often confused with the winter one. After 30 straight days of unoccupancy — at any time of year — water, vandalism, and theft coverages start falling away. The triggers most people don’t think about: the house is sold and closing in 45 days, the snowbirds are away for the winter, an inherited property is in probate, the tenants moved out and the new ones haven’t moved in. The fix is a vacancy permit. Arrange it before the home goes empty. Call us the day you know the property will sit empty. Not day 29.

Poly-B plumbing. BC homes built between 1978 and 1995 often have polybutylene pipes in them. They fail. BC carriers are tightening on poly-B every year — some apply a higher water-damage deductible, some put a deadline on replacement, some refuse the policy entirely. If you bought a home from this era, check the basement before your renewal arrives.

The strata deductible problem. More than 60% of BC strata corporations now have building deductibles over $50,000 — up from 15% in 2020 (BCFSA). Section 158(2) of the BC Strata Property Act lets the strata recover its building deductible from the unit owner whose unit caused the loss. No negligence required. The dishwasher hose breaks, your unit floods three other units, the strata’s deductible is $50,000 — that’s a $50,000 bill landing on you, regardless of fault. Most BC condo owners’ loss-assessment limits aren’t sized for it.

Wildfire binding restrictions. When BC has active fire events, carriers stop writing new policies or adding coverage in the affected zones. If you’re closing on a property during a binding-restriction window, you can find yourself with a mortgage that requires insurance and no insurer willing to write it. The pre-fire-season bind window (April to May) is when smart buyers lock in. FireSmart certification matters for properties in exposed areas.

Oil tanks. Underground oil tanks are an environmental liability before they’re an insurance one. Most BC carriers require certified removal before they’ll write or renew. If your property has, or ever had, an oil tank — flag it before you call.

If any of these apply to your home, a 30-minute review tells you whether your current policy is built for it.

Get a Second Opinion on Your Current Policy →

What is never covered on a BC home policy.

A home policy is not a maintenance contract. Predictable and preventable events aren’t covered — no matter how much you pay. The big ones:

- Earth movement. Landslides, earthquakes, other earth movements. Damage from a fire caused by earth movement is covered. Earthquake itself can be added — see the glossary.

- Freezing of indoor plumbing. Treated as preventable. Frozen pipes aren’t covered if the home is unattended more than four days in heating season without shutting off the water or having someone check the heat.

- Freezing outside the home. Melting or moving snow and ice, heaving frost. Roof ice-damming coverage can sometimes be added — ask.

- Intentional application of heat. Clothes shrunk in the dryer or scorched by an iron. If the dryer catches fire and spreads, the fire damage is covered. The shrunken clothes are not.

- Damage by insects and rodents. Pest damage is a maintenance issue.

- Food spoilage in freezers. Commonly excluded, especially on seasonal policies. A narrow add-on is sometimes available.

- Pollution. Not covered.

- Property acquired illegally. Not covered.

- Criminal or intentional acts of the policyholder. Not covered.

- War, terrorism, nuclear risks. Not covered.

- Gradual deterioration and normal wear and tear. A rotting deck, an aging roof, worn shingles. Maintenance, not insurance.

How to lower your premium. Honestly.

Most BC homeowners are claiming two or three of the discounts they qualify for. Plenty qualify for five or six. On a typical detached policy, that gap is hundreds of dollars a year.

The biggest levers are usually the boring ones. Bundle home and auto. Stay claims-free. Pay off the mortgage. Hit 55. Pay annually instead of monthly.

The property updates that move the needle: a water leak detection device with automatic shut-off (manufacturers report up to 96% reduction in non-weather water claims), monitored fire and burglar alarms, and FireSmart Wildfire Mitigation Program certification.

Now here’s the caveat nobody else mentions.

Install the device for the discount, then actually use it. A water shut-off valve installed and then turned off, or an alarm system that’s been deactivated, can both lose the discount AND give the carrier grounds to deny the claim — because the carrier wasn’t told about the change. The discount is the carrier paying you to manage the risk. Keep managing it.

Independent broker, direct writer, or call-centre.

Three ways to buy home insurance in BC. Each works for someone, and most BC homeowners are with whichever one they ended up with by accident.

Independent broker. Shops your policy across multiple BC carriers in one conversation. The same house gets different prices from different carriers on the same day — that’s what shopping the market actually means. Best for homes with any complexity: prior claim, older systems, strata coordination, hard-to-place risk.

Direct writer. An online-only carrier selling its own product directly. Fast quote, clean process, often the cheapest answer for a simple newer home with no underwriting complications. Less effective when the home needs anything outside the standard template.

Call-centre operation. A large brokerage with centralized phone-based service. Scale, scripts, and a different agent every call — fine for renewals on an uncomplicated file, harder when a claim needs continuity.

So which one’s right for your home?

If your property is simple, newer, claims-free, and you don’t mind the online flow: a direct writer can be cost-competitive. If your file has any complexity, or you want a name on the file when something goes wrong, the multi-carrier independent route often gives you the better review. Neither is wrong. The wrong move is staying with whichever you ended up with by default.

What working with Prime looks like.

Prime is a family-owned independent insurance brokerage in Surrey. Family-run since 1994. Multiple BC home insurance carriers, shopped in one conversation.

You’ll know who’s on your file. Prime is a family-owned brokerage, family-run since 1994. Your home insurance is handled by a dedicated, licensed advisor — Kuljeet or Seema — two of the twelve advisors across the brokerage. Someone you can call by name. Someone who can pick up the file tomorrow when life happens. Not a different agent every time you call. Not a queue.

We work in English, Punjabi (ਪੰਜਾਬੀ), and Hindi (हिन्दी). If it’s easier, bring your declarations page to the counter and we’ll read it with you in the language you’re most comfortable using.

We’re open Monday to Friday until 9pm, Saturday until 6:30pm, and Sundays and stat holidays from 10am to 5:30pm.

Call 604-582-0557 or email your declarations page to [email protected].

Here’s how the first conversation goes. You bring your declarations page. We walk through it line by line — what’s covered, where the gaps are, what your discount stack looks like, and whether the BC market has a better fit for your home. Thirty minutes, usually less.

Honest answer either way. If your current policy is the best fit for your home, we’ll tell you that and thank you for coming in. If we can do better, we’ll show you what — and we shop the BC market across multiple carriers in one conversation. You don’t fill out five online quote forms. We do the running.

The BC carriers we shop for you.

Multi-carrier access is what makes the second opinion useful — the same house gets different prices from different carriers on the same day. Prime works with:

- Wawanesa Insurance

- Optimum General Insurance

- Family Insurance Solutions

- Peace Hills Insurance

- Max Insurance

- BECK Insurance

- Forward Insurance

- Chubb

- Northbridge / Onyx

- Lloyd’s specialty markets

We also place hard-to-place risks through MGA channels — useful when the file has a prior claim, an unusual structure, or a coverage shape standard carriers won’t write.

Get a second opinion on your current policy.

Bring your declarations page. We’ll read it line by line in 30 minutes, tell you what’s covered and where the gaps are, and either confirm your current policy is the best fit — or show you a better one. No obligation. Honest answer either way.

Prime Insurance 150-8888 152A St, Surrey BC V3R 0V7Mon–Fri 8:30am–9:00pm · Sat 8:30am–6:30pm · Sun & Stat Holidays 10:00am–5:30pm

English · Punjabi (ਪੰਜਾਬੀ) · Hindi (हिन्दी)

Get directions →

The BC home insurance terms most homeowners get wrong — and where coverage problems usually start.

If no one has walked you through these, your policy probably has gaps. Each one has tripped up BC homeowners at claim time. If you’re not sure how yours is written, bring it in and we’ll go through it together.

Replacement cost

What it would cost to rebuild your house today, with today’s labour and materials. Not what you paid for it. Not your BC Assessment. Not market value. If this number is wrong on your policy, every other coverage is built on a wrong foundation.

Call to review yoursGuaranteed Replacement Cost

Your house burns down. The rebuild comes in 15% over your policy limit because construction costs moved. On a Guaranteed Replacement Cost policy, the carrier still pays. On a standard policy, you pay the overage. Most high-value products include this. Most mainstream policies don’t — and many cap the bylaw portion.

Call to check yours30-day vacancy rule

Every BC home policy restricts coverage after 30 consecutive days of vacancy. Water damage, vandalism, and theft are the first coverages to fall away. If the property will sit empty, call us on day one, not day 29. “Unoccupied” (furnished, short-term empty) and “vacant” (empty with no return date) are treated differently by carriers, and the line between them matters.

Call before it’s vacantLoss assessment

Your strata has a major claim and the corporation’s insurance isn’t enough to cover the whole loss. The gap gets split across every unit owner — sometimes thousands per unit. Loss assessment coverage pays your share. Most policies default to $1,000 or $2,500. For most BC stratas today, that’s not enough — raise it. (Condo owners: see the condo insurance page.)

Strata owner? Call usOverland water vs. sewer backup

Two different coverages — and most homeowners think they have both when they have neither. Overland water is water coming in over the ground from heavy rain, snowmelt, or a creek overflowing. Sewer backup is water coming up through your drains and toilets. Your policy includes neither by default. Both matter in the Lower Mainland.

Which do you have?Water escape

What happens when plumbing, appliances, or hot water tanks fail inside the house — a burst pipe, a washer hose that splits overnight, a dishwasher that leaks into the subfloor. This is covered on a standard BC policy, unlike overland water or sewer backup, and it’s the most common claim category. Two catches: damage from hot water tanks over 15 years old is often excluded, and freeze damage in an unattended home follows the four-day rule.

Check your water coverageService line coverage

The water, sewer, gas, and electrical lines running from the property line to your house. Most BC homeowners don’t realize they own these — until one breaks. One excavation to find and replace a broken line runs $5,000 to $15,000. The add-on costs a fraction of that. Most standard policies leave it out.

Ask about this add-onEarthquake deductible buy-down

BC earthquake deductibles aren’t a flat dollar amount — they’re a percentage of your building’s insured value, usually 10% to 20%. On a $1.2M home insured for $1M, that’s between $100,000 and $200,000 out of pocket before the policy pays a cent. A buy-down endorsement lowers the percentage. Availability varies by postal code, so call us with your address.

Check availabilityBylaw coverage

If your house is destroyed and you rebuild, your municipality makes you rebuild to today’s code — not 1978’s. Seismic retrofits, updated electrical, modern insulation, new plumbing. That adds 10% to 25% to the rebuild cost. Bylaw coverage pays the overage. Most policies cap it. Older homes need this checked.

Check your bylaw limitFour-day rule

Away from home more than four consecutive days in winter? Either shut off the main water supply, or have someone physically check the heat is running daily. If you don’t, and a pipe freezes and bursts while you’re gone, the water damage isn’t covered. This exclusion lives in every BC home policy.

Travelling? Call firstScheduled personal property

Your regular policy caps certain categories — jewellery around $6,000, bikes around $2,000, cameras around $2,500. If your engagement ring is worth $15,000 and it’s lost, the policy pays out at the cap, not the ring. Scheduling the ring (sometimes called a “floater”) covers it for full value, worldwide, with broader perils. Receipts and an appraisal required.

Schedule an itemUmbrella liability

Your home policy covers up to $2M in personal liability and your auto policy another $2M. For most BC homeowners that’s enough. For some — landlords, pool owners, waterfront, higher-net-worth households — it isn’t. An umbrella policy stacks another $1M to $10M on top of both, across all your property. Direct writers rarely offer one. We do.

Ask about umbrellaFrequently asked questions.

Is home insurance required by law in BC?

No. It’s required in practice because your mortgage lender demands it. Without insurance, you’re personally responsible for any rebuild, replacement, or liability cost — which for most BC homeowners runs into six or seven figures.

How much is home insurance in BC?

Premiums vary by property. Most BC detached policies fall between $1,200 and $2,500 a year, with policies above and below that range. Your number depends on rebuild cost, location, claims history, age of major systems, and which optional coverages you carry.

Why did my premium go up if I didn’t make a claim?

Your premium reflects industry-wide losses, not just your own claim history. Canadian severe-weather losses hit $8.55 billion in 2024, the costliest year on record (IBC). BC premiums rose 5.89% on average in 2025. Your number can rise even if your file has been clean.

Should I switch carriers every year to chase the cheapest rate?

No. Switching costs you the loyalty discount, takes claims-history transfer effort, and burns time. A multi-carrier independent brokerage can shop your policy in one conversation, without starting fresh at each carrier. The right move is a market check every second or third renewal. Not a switch every year.

Can I get a quote without committing to switch?

Yes. A 30-minute review and quote is no-obligation. If your current policy is the best fit, we tell you that and you stay where you are. If we can do better, you have a real comparison to make a real decision on.

Does my standard policy cover earthquake?

No. Earthquake is excluded from every standard home policy in Canada and must be added as optional coverage — usually as an endorsement. BC deductibles are percentage-based, typically 10% to 20% of the insured value. A buy-down endorsement can lower the percentage where it’s available.

Does my policy cover overland water or flood?

Not by default. Overland water coverage is an optional add-on, and availability varies by postal code. Homes in Cloverdale and parts of the Fraser Valley flood plain may not qualify with domestic carriers; Lloyd’s syndicates and other specialty markets sometimes write the risk on different terms.

Is sewer backup automatic on my policy?

No. Sewer backup is an optional add-on that covers damage when sewers, drains, or a sump pump back up into your home. It’s different from overland water. Both are worth having in the Lower Mainland.

What about the service lines running into my house?

Most BC municipalities hold you responsible for the underground water, sewer, gas, and electrical service lines from the property line to the house. A standard policy doesn’t cover repair or replacement of these. Service line coverage is an inexpensive add-on that does.

What happens if my home sits vacant while I sell it?

Most BC policies have a 30-day vacancy rule. After 30 consecutive days without written permission from the insurer, standard coverage restricts or drops. You need a vacancy permit or a standalone vacant-dwelling policy to stay covered. Call us the day you know the property will sit empty, not day 29.

What about insurance while my home is being built or renovated?

New builds and gut renovations sit outside a standard homeowner policy — those need builder’s risk (course of construction). Minor renovations can stay on your existing policy if you disclose the work. Larger renovations may need a renovation add-on. Call us before the permit is issued.

Does home insurance cover damage from wildfire?

Yes. Wildfire is covered under the standard fire peril, and evacuation expenses fall under additional living expenses (usually requiring a mandatory evacuation order). During active wildfire season most carriers impose a binding moratorium — they stop writing new policies within a set radius of an active fire. Zones vary by carrier, which is why a brokerage with multiple markets can sometimes still place coverage when a direct writer has closed the door. Call before the smoke comes, not during.

Can I bundle home and auto for a discount?

Sometimes. When the best home carrier is also the best auto carrier, the multi-policy credit applies. When they’re different, the split often beats the bundle. We run the numbers both ways and tell you which costs less.

My previous insurer non-renewed me — can Prime still place the policy?

Usually, yes. We have access to specialty markets and managing general agents that write risks standard carriers won’t. Premiums are higher, but most “uninsurable” risks are actually placeable. Bring us the non-renewal letter and the previous declarations page.

Is my $1M+ home covered properly on a standard policy?

Probably not. Homes above about $1M to $1.5M replacement cost are better served by a dedicated high-value product — guaranteed replacement cost, higher built-in liability, worldwide coverage, dedicated claims service. We place these with Chubb, Northbridge/Onyx, and Lloyd’s specialty syndicates. See the high-value home insurance page.